Q4 2023 San Francisco Multifamily Report

The 2024 outlook for San Francisco Multifamily is filled with promising signs.

San Francisco Multifamily Ends the Year on a High Note Despite Obstacles

2023 marks a year where San Francisco’s multifamily market has been challenged by tightening lending conditions, low office attendance, and unrest over homelessness and crime. Yet, there are many promising signs of growth and recovery. Federal Reserve interest rates have plateaued with consensus of rates lowering in 2024, retail employment in the city is up year-over-year, and neighborhood commercial corridor vacancy has decreased. APEC conference showed the world that a clean and safe San Francisco was possible and the multifamily market has reflected this optimism. Sales velocity has seen steady growth in Q2-Q4 and rents have recovered to pre-pandemic levels.

District-by-District Analysis - Trailing Twelve Month Average/Total as of 12/31/2023

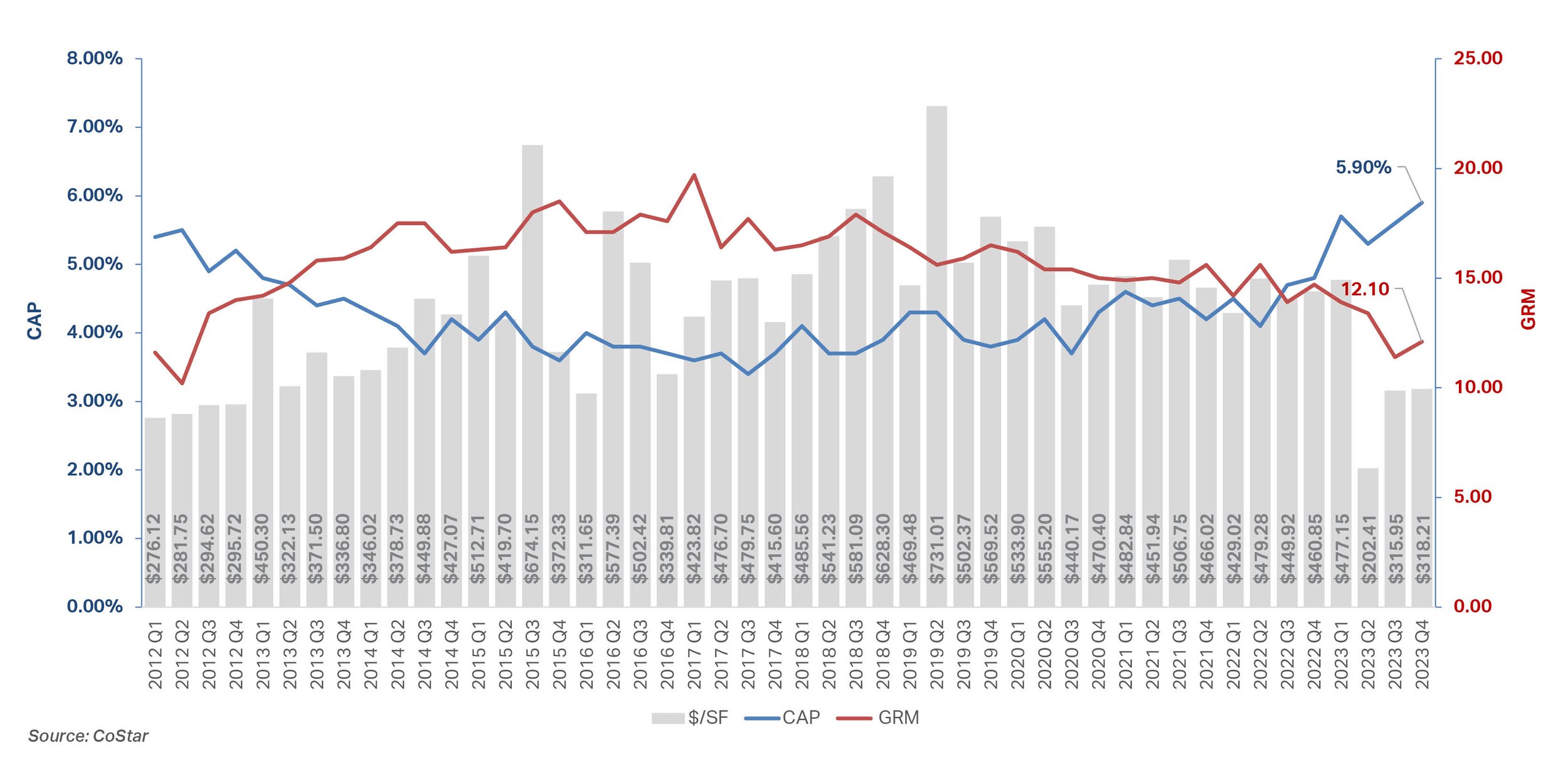

Cap Rate | $/SF | Total Transactions - 5+Unit Multifamily Properties - Source: SFAR MLS

At the end of 2023, we saw cap rates decompress to 5.9% in correlation to the Federal Fund Rate of 5.3%. Transaction velocity decreased with the defaulting of several regional banks, which tightened lending for several months. However, rents have remained strong as home-buyers have been priced out and are forced to rent. Strong rents in combination with falling interest rates increased sales volume in Q3 and Q4. Market sentiment is positive and well-priced real estate continues to sell. LL CRE is optimistic for 2024 and we expect sales volume to return to pre-pandemic levels.

Cap Rates, $/SF, and GRM, 5+ Unit Properties

Multifamily Vacancy Rate & Asking Rents

Transaction Volume and Active Listings

Federal Funds Rate, 30-Year Mortgage Rate, and 25-Year SBA504 Loan Rate

This report has been prepared solely for information purposes. The information herein is based on or derived from information generally available to the public and/or from sources believed to be reliable. No representation or warranty can be given with respect to the accuracy or completeness of the information. Compass and LL CRE Group disclaim any and all liability relating to this report, including without limitation any express or implied representations or warranties for statements contained in, and omissions from the report. Nothing contained herein is intended to be or should be read as any regulatory, legal, tax, accounting or other advice and Compass/ LL CRE Group does not provide such advice. All opinions are subject to change without notice. Compass and LL CRE Group makes no representation regarding the accuracy of any statements regarding any references to the laws, statutes or regulations of any state are those of the author(s). Past performance is no guarantee of future results.

Contact us for more market information or multifamily investment portfolio consultation

Brian Leung

Senior Vice President

Lic. 01203473

415 278 7838

Brian@LL-CRE.com

Jeremy Lee

Senior Vice President

Lic. 01951309

415 988 9719

Jeremy@LL-CRE.com

Carla Pecoraro

Associate

Lic. 02019669

415 312 8901

Carla@LL-CRE.com

Chris Leung

Associate

Lic. 02194279

415 828 9108

Chris@LL-CRE.com